What a month it has been. At the end of January, I sent a market commentary. One month later, the most meaningful change is the Russian rumors became headlines as they try to re-establish their Imperial borders

The equity markets during the first two months of 2022 have been, so far, less than stellar. Good companies, businesses with strong earnings and terrific future growth potential, tossed aside as prices have declined from just two months ago. What happened and why? Do I need a new strategy for the Russian Roller Coaster? No, you do not.

By now, the world knows that Russia launched an attack on Ukraine. The markets have been uneasy for weeks while this was simmering. One global repercussion is China now finds itself in the unenviable position of backing up their new bestfriend while keeping the US relationship intact.

Russia is one of the world’s largest oil producers, providing 10% of all global needs. The huge spike in oil prices during the preceding months directly benefits Russia, as newfound billions in revenue pour into their Treasury and military. It<br>

goes a long way help pay their internal unfunded expenses, such as salaries for teachers, miners, municipal workers, and soldiers. The longer the uncertainty exists regarding their true end game, the longer oil prices remain severely elevated, a huge Putin goal. As a reference, the Russian Ruble is worth less than a U.S. penny.

Of course, the invasion spooks investors, mostly as an automatic reaction. Still, if your home suddenly lost value, do you rush to sell? Never forget that driving most stock market trading are powerful institutional computer servers running automated trading programs. We have seen this before.

Everyone is aware inflation has increased to levels we have not seen in decades. People notice this at supermarkets where the cost of certain items look like price-gouging, or when they fill the gas tank.

Inflation is also attributed to supply chain issues where many goods imported from other countries, are simply delayed, or discontinued. Other products produced in the US have endured delivery problems, further keeping inventories slim. Often, it boils down to a truck driver shortage or the sole forklift operator at the warehouse is out sick. Businesses are also raising prices to cover the costs of hiring and retaining their staff. It is usually the end-user consumer that pays for that. Recall the ship that blocked the Suez Canal that started all the supply-chain issues. That was March 2021. Time flies.

We work hard to make sure we are solving future financial issues, not feeding them. Inflation has now clocked the highest rate in forty years. Even if the Federal Reserve discounts their version, inflation is now averaging more than 5% annually. So, it makes sense that we need to earn more than 5% to keep moving forward. In most places, food and energy costs are increasing faster than 5%. One year ago, gas was $2.40/gallon. In Los Angeles gas is approaching $4.75/gallon and $5.00 gas seems inevitable. Yes, $75 – $100 to fill up the car.

My January commentary noted Vladimir Putin has little or nothing to do with Home Depot’s stock. Yes, his actions create a ripple effect in the markets with uncertainty and stock price volatility. This is not cause and effect, and not entirely rational. Recall the US economy is ten times the size of the Russian economy. Despite the Ukraine invasion, Home Depot is still open for business, my Verizon cell phone works fine, and I can still use a Visa debit card. We instinctively know this, but sometimes forget.

We look for potential growth out of necessity. The Ten-year treasury bond yields approximately 1.75%. With future interest rate increases, that yield moves higher for those willing to wait a decade. Consumers will not notice much of a difference on their bank statements.

Market swings now cause investors to contend with a new issue: whiplash. Down 850 points in the morning, and up nearly 100 points in the afternoon. Still, the stock price has little or nothing to do with the company business.

We invest for the longer term. Each person has a different definition of “longer,” but it is always more than 12 months. We invest to grow investment principal because investors will need it. The headwinds of taxes, inflation, RMD distributions (required minimum distributions from non-Roth retirement accounts) depreciation and longevity force us to keep capital moving faster and further than these financial impediments. By itself, inflation functions as an after-tax…tax.

Well-managed companies are good businesses where we want to be part-owners. Ask any of the employees of Amazon, Google, Apple, McDonalds, or Microsoft. What does Putin’s invasion have to do with the day-to-day operation of these companies? Absolutely nothing. Sure, scary headlines can cause stock prices to fall and the that’s the reason we reinvest dividends–to capture those lower prices. Could stock prices further decline gradually, or through a sudden large drop? Yes, it’s possible. Warren Buffet would say that is the exact time to fill the shopping cart, not run and hide. He doesn’t cut the flowers to leave the weeds.

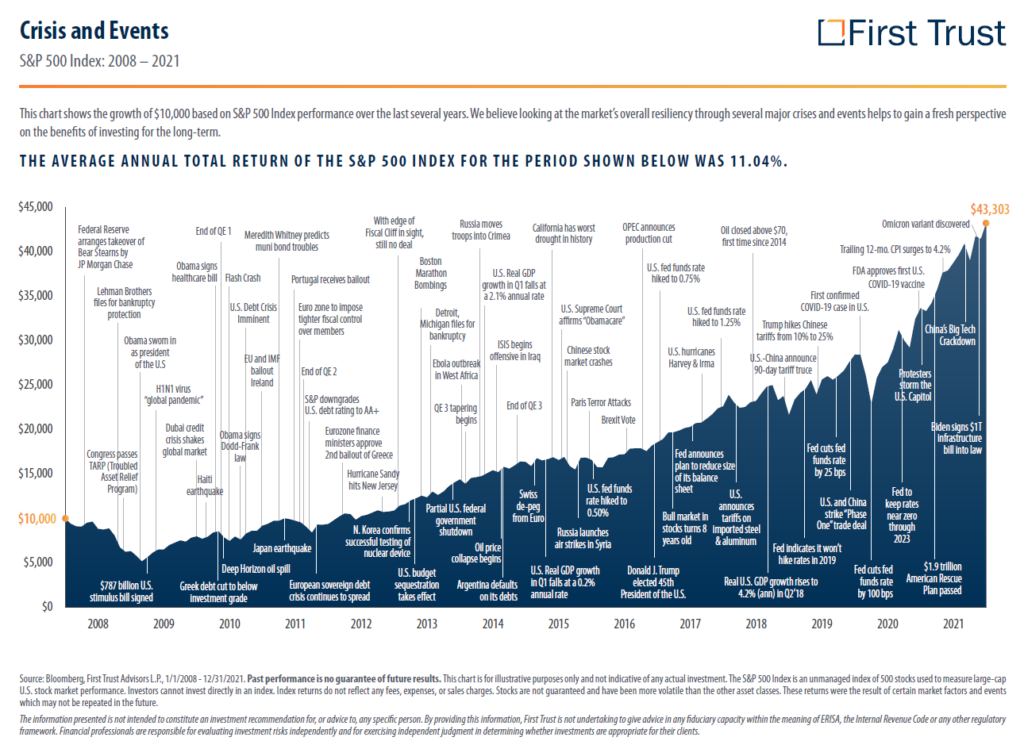

The attached third-party charts illustrate the long-term nature of investing. Could balances decline before potentially growing to new, record highs later? Quite possibly yes. Have we seen this before? Yes, and we will see it again. In March 2020, when Covid began, stock prices plummeted. It was downright ugly. Everyone is now glad they stopped looking and by year-end, the gains were impressive. 2021 was much of the same, and year-end balances were for almost everyone at record levels. We are now only two months into 2022. Be patient.